Is A Home A Good Investment in Early 2023?

Background

I’m considering buying a home for the first time, and in this article I detail out my thoughts about the process. Hopefully you learn something along the way, too. I have no affiliate links to sell you, no investing app referral codes, and no books or downloadable PDFs for sale that might skew my interest.

Setting the Scene

I live in Austin, and so for this article I’m focused on the greater Austin area. For future readers, consider the timeframe of early 2023: housing prices are coming down from an all time high. Mortgage rates have doubled from what they were just a few months ago. Hordes of tech employees are being laid off. Inflation has been horrendous over the past year. Mainstream media news articles talk about an upcoming recession - but its pretty clear we are already in one.

I currently live in a BJJ Dudebro house where I am splitting a 4 bedroom, 3 bathroom, 2200 sqft house with 3 other people. My rent is cheap. If I were to buy a house, I’d be renting out the other bedrooms. I’m not trying to go up or down in scale, I just want the same setup but where I’m the landlord. This has the added benefit of making the math simple.

I’m looking for the same setup: a 4 bedroom house with over 2,000 square feet. My price range is 400-500k. I’ve done the leg work. I have enough in investments for a 100k down payment. I have a solid enough income where I could pay the mortgage on my own if I had to, I have an emergency fund I can dip into, I have no debt, and my credit is high 700s.

Key considerations for me in buying a home

Do my mortgage payments actually turn into equity?

Would I rather invest in a home that I buy, or in a diversified portfolio?

How will my tax situation change?

Cash flow analysis and life planning

Do my mortgage payments actually turn into equity?

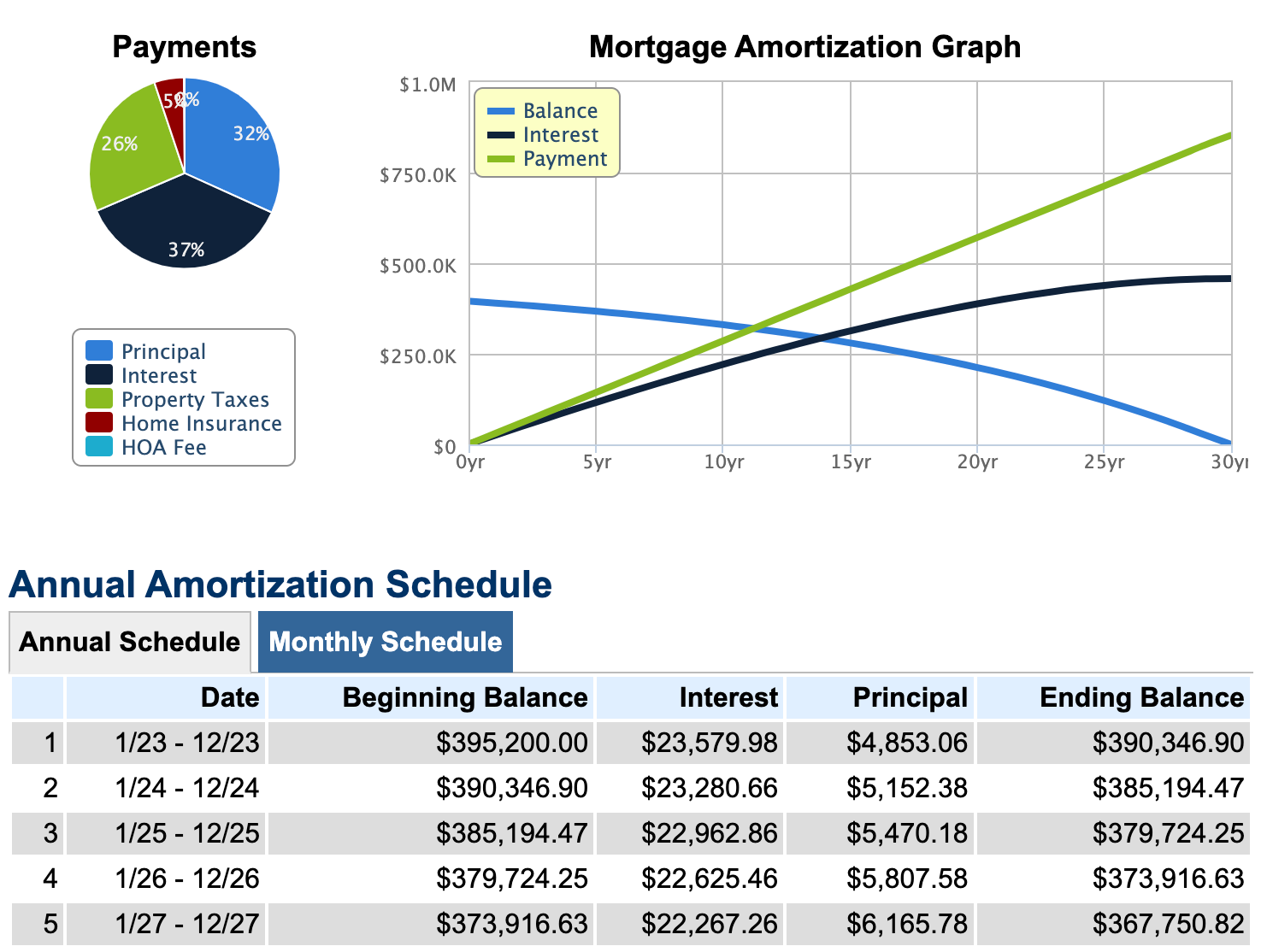

In order to make the rent vs buy comparison apples to apples, I first need to know how much equity I’m building the home.

On the high end of the price range, we have a listing like this one with these parameters

$494k home with 4 beds, 3 bathrooms. 2600 sq ft.

With 20% down @ 6%, Zillow’s estimated monthly cost is $3,500

With the current rental market I could expect $2,500

I can see that in the first 5 years, I’m putting roughly $5.5k/yr into the home in equity. The rest is wasted on interest.

In monthly terms, at the start I’m paying $393 into equity and by the end of year 5 I’m at $528.

Assuming the house price and inflation remains the same (which is crazy), that means I’m burning ~$1,000/mo by owning it. Plus I get the negatives of

Taking on maintenance and repairs,

Having an illiquid asset instead of diversified portfolio of stocks or [insert asset class here], and

Having to pay the mortgage even if I quit my job, lose tenants, or move.

In this apples to apples scenario, my cashflow is essentially net negative $600/mo (extra $1000 per month minus ~$400 going into equity) and I take on a huge amount of risk. This is why some millionaires argue that you should just perpetually rent, and invest in the stock market or wherever else. I burn $600/mo in interest that’s in excess of what rent would be, and that $400 that’s going into equity of a single home could be going into a diversified REIT that’s spread out across thousands of homes.

Now let’s talk about the upside

What I do get with buying a home is a leveraged investment. If the home value goes up but I don’t add much equity, I can still profit a lot. At the same time, I stand to lose a lot if the home value goes down.

Second, since I’m the landlord, I can make improvements to my house, which means increased home value and rental income. New floors? Kitchen island? Garage built-in cabinets? Solar panels? Backup power for the next major grid outage? These are all things I can do with time, YouTube university, and the occasional professional contractor. I can spend free time doing projects that will yield a return.

A non-monetary benefit is that I am now his majesty, lord of the land, and nobody can tell me what to do with my property besides the HOA, city ordinances, state and federal government. If I want to knock down a wall to make space for jiujitsu mats, turn the garage into a metal forge, build a sauna in the backyard, rent out the tool shed to some college kid, or make short-term rental arrangements, I DON’T have to bend the knee to seek my landlord’s approval. For me personally, this is a HUGE benefit and is worth a significant premium.

Marry the house, date the rate

This is a popular idiom among realtors to get you to buy a home regardless of the current interest rate, but it has some truth to it. Assuming interest rates will stay the same for 30 years isn't representative of reality.

In Texas I’m only locked into my rate for a year.

If interest rates go down, then there will be an opportunity to refinance the home and lower the monthly payment.

If interest rates go up, then over the short term housing prices go down (lowering rental income but also property taxes) but over the long term, such as 1970s style stagflation, the value of the loan goes down with inflation. Assuming my income increases with inflation (which could be a bold assumption for a salaried employee), this is a win.

Would I rather invest in a home that I buy, or in a diversified portfolio?

If both the stock and housing market returns are the same (again, crazy) then I’m weighing the benefits of either

Being a homeowner: I'm my own landlord, and I now have opportunity to do work / invest in my home. Excess income from my job could be invested in either the home or in other markets. On the downside, I take on huge risk by owning a home.

Being a renter: The extra money I save in renting vs owning a home can go into more investments. I’d own a highly liquid and diversified portfolio, have nomad capabilities of moving wherever I want with a breeze when my lease is up, but at each place I’d have to bend the knee to my landlord. True story: in Southern California, real estate conglomerate Irvine Company raised rents on new leases by 50% when the pandemic hit.

Risk in the Stock Market

The stock market is a lot riskier than what the standard models predict. A diversified portfolio is full of a bunch of terribly run companies that you wouldn’t want to buy compared to a solid piece of land with growth potential.

See my previous post that critiques Modern Portfolio Theory. The TLDR is that stock markets are riskier than the standard models and analysts would have you believe, and the true risk is hard to calculate (which is why the statisticians still cling to their broken tools). I am taking this unorthodox viewpoint into account when weighing it against the fact that buying a singular home is also a huge risk.

“Value” in the Stock Market

Go take a look at what’s in the S&P500 (link) and ask yourself which of those companies you’d buy. There’s plenty of garbage in there that’s overpriced AND poorly managed.

If you've read Benjamin Graham's The Intelligent Investor, you know Price to Earnings ratio is a valuable indicator as to whether or not a company is overbought/oversold relative to its intrinsic value. Stocks with a PE ratio of under 30 are generally considered worth buying (originally 13.3, this source adjusts for today's numbers). You'll see many companies with PE ratios > 60, like GE (121), META (106), Microsoft (87), CarMax (72), and so on. According to Graham, these are all overpriced. (But one could argue that the Austin housing market is also overpriced).

So, home + stocks, or stocks + more stocks?

Which would I rather have?

A diversified portfolio of assets that I don’t have to manage, but has risks I can’t control

Having a lot of money tied up into one house, that could perform wildly different than the general market. I have to pick the home, improve it, and maintain it.

In my mind, I opt for the later. It gives me more control and responsibility over the situation. I can’t prevent a global recession, but I can pick a home in a neighborhood that might grow EVEN IN a recession. Lots of people are moving to Austin from more expensive locations, so it’s not a totally unrealistic idea to think my inflation adjusted returns on my home value will be substantially higher 10-20 years from now.

How will my tax situation change?

I’ll benefit from itemizing my deductions

The standard deduction for singles in 2023 is $13,850 [source].

I can deduct the interest on my mortgage from my taxes [source].

According to the earlier calculator example, I will pay $22.3-23.6k in interest each year for the first 5 years on a $394k 30-year loan with 6% interest (see graph above).

This means I’ll see get an extra ~8.5-9.5k above the standard deduction, and so my taxable income is lowered by that amount.

At a $150,000 income, my federal taxes would be $24,172 instead of $26,278 [tax calc].

I essentially get a $2,000 bonus thanks to mortgage interest being deductible (although toward the end of my loan my interest will be zero). This works out to $167 per month.

Rental income

Rental income is taxable. So instead of sharing a $2,500/mo house with roommates, I collect income from them and must pay taxes on it. This is a big negative.

If my roommates paid $800/mo, that’s an income of $2,400/mo. I’m left paying $1,100/mo on a $3,500/mo house payment.

That’s $28.8k/yr in income. My income would go from $150k —> $178.8k.

My federal tax bill would go from $26,278 —> $33,640

This is $7,362 more in taxes

I pay an extra $576/mo to Uncle Sam.

$576/mo income tax - $167/mo taxes saved from deductions = $409/mo more in net taxes

Deductions

Repairs and Improvements - I can deduct repairs but not capital improvements. Improvements can be deducted through depreciation (though this lowers my tax basis for the home and increases taxes due when I sell). See more in the IRS guidelines: https://www.irs.gov/businesses/small-businesses-self-employed/tips-on-rental-real-estate-income-deductions-and-recordkeeping

Texas homestead exemption - My property taxes are calculated as if my home’s value was assessed $40k lower as long as the home is my primary residence. $40k homestead exemption * 2.21% property tax in my area = $884/yr =~ $74/mo less in property taxes. The $40k applies to school taxes, but there are also benefits towards other property taxes.

The 1031 exchange - This one is HUGE. I can defer my capital gains taxes with real estate. This is essentially the real estate-equivalent of a Roth IRA, except I can cash out any time I want. There’s plenty of content about this on the internet here.

Cash flow analysis and life planning

Take all of these numbers with a grain of salt.

I’m not going to assume I’m going to live in the same home for 30 years.

I’m young. I’m not going to have roommates for 30 years. Whether I’m renting or buying, my living situation will change at some point as I get older.

I have to account for kids and starting a family. As a 26 year old, I see many of my friends who were dead set on not having kids changing their minds and opening up to the idea of having a family. I’m personally starting to shift more this way. I consider it a possible scenario and want to illustrate it financially. I’m definitely not having roommates when I have a kid.

Summary

When looked at through a 5 year lens, does buying a house make sense right now? Strictly financially speaking, no it does not. I could be in the negative for even longer than that.

You could argue that homes are overpriced and rates are too high, and we’re headed into a recession so we should expect values to continue to go down. At the same time the government is continuing to print money so we should expect interest rates to continue to go up. Buying in a down market is like trying to catch a falling knife.

On the flip side, if the market was going up, then I’d continue to be kicking myself for not buying sooner. I’d be wanting to buy after the peak, at the next bottom (whenever that is) I’ll have to consult my crystal ball.

A single house could do much worse or better than a diversified REIT portfolio.

When added with other non-monetary benefits, however, I can justify the cost. Taking a 10-20 year long term view, the odds I will be in the red on a house in a booming area like Austin are low. I could take a big hit financially, but it’s a bet I’m willing to take. I want my own damn place, and it’s just financially sane enough for me to bite the bullet.