The Big Thing the Personal Finance Community Gets Wrong

Why maximizing frugality and dumping your savings into the market is a risky idea

Why is frugality so common?

One of the core tenets of the financially independent, retired early (FIRE) community is to obtain a big enough balance in your portfolio / net worth so that you can retire off of investment income alone. The idea is that if you keep your withdrawals below your yearly returns on investments, then you no longer need to work. 3-4% is a common recommendation for those who are younger.

There is a very common temptation to focus on frugality and how to curb expenses, rather than focusing on how to increase wealth generation. After all, spending less money is something you can do right now, you can keep the same job, and it doesn’t cost you anything. All you need to do is say “no” to more stuff. You don’t really need to do anything. Cut out expensive habits, swap eating out for cooking your meals, travel less, cut coupons, pay down your debts and you can slowly make your way to millionaire status. After all, that’s what Thomas J. Stanley, author of The Millionaire Next Door and Stop Acting Rich…and Start Living Like a Real Millionaire, would have you wanting to think. There are more millionaires that are teachers and accountants than there are mega-millions entrepreneurs.

The lower your cost of living, the less money you’ll need in your portfolio in order to obtain FIRE status. While reducing superfluous spending is important, what I’m saying is it’s not the ONLY thing that is important. There is only so much expense you can cut before you are living like a monk, two steps above homelessness. If that kind of lifestyle sounds unappealing to you, then you are in the right place. If I am going to be saving up to drive a Lamborghini, I want to be young enough to actually enjoy it when I drive it . If I want a 4 bedroom 2,000 square foot house in a mediocre suburban area by the time I retire, then I’ll follow Stanley’s advice.

How big of a portfolio do you need and how long will it take to get there?

What does it take to retire early? For easy math, let’s say our monthly costs are $5,000. Our yearly cost is $60,000. With a “safe” portfolio withdrawal rate of 4%, we need a portfolio size of 60,000/0.04 = $1,500,000.

With a median household income of $79,212 in November 2022 [source], we’ll assume $80,000 for easy math. We’d expect to save $20,000 a year.

The commonly accepted ballpark figure for inflation-adjusted returns on the stock market is 6-8%. Take note we’re currently experiencing high inflation and in a bear market, if the 1970s stagflation serves any example, we may not see returns above inflation for a long time to come.

Optimistic & Pessimistic Calculations

So how long does it take for us to get to $1.5M, saving $20k a year and getting 6-8% returns? We’ll use an amortization table to track compounding interest alongside contributions throughout the process.

Link to calculator with these parameters

Result: It takes 25 years to get to this point! With 6% returns, it takes 29 years. More scenarios further below.

But is this realistic?

So on the surface, it certainly sounds doable, but keep in mind these are only very rough estimations. Any certified financial planner will tell you that past performance is no guarantee of future performance.

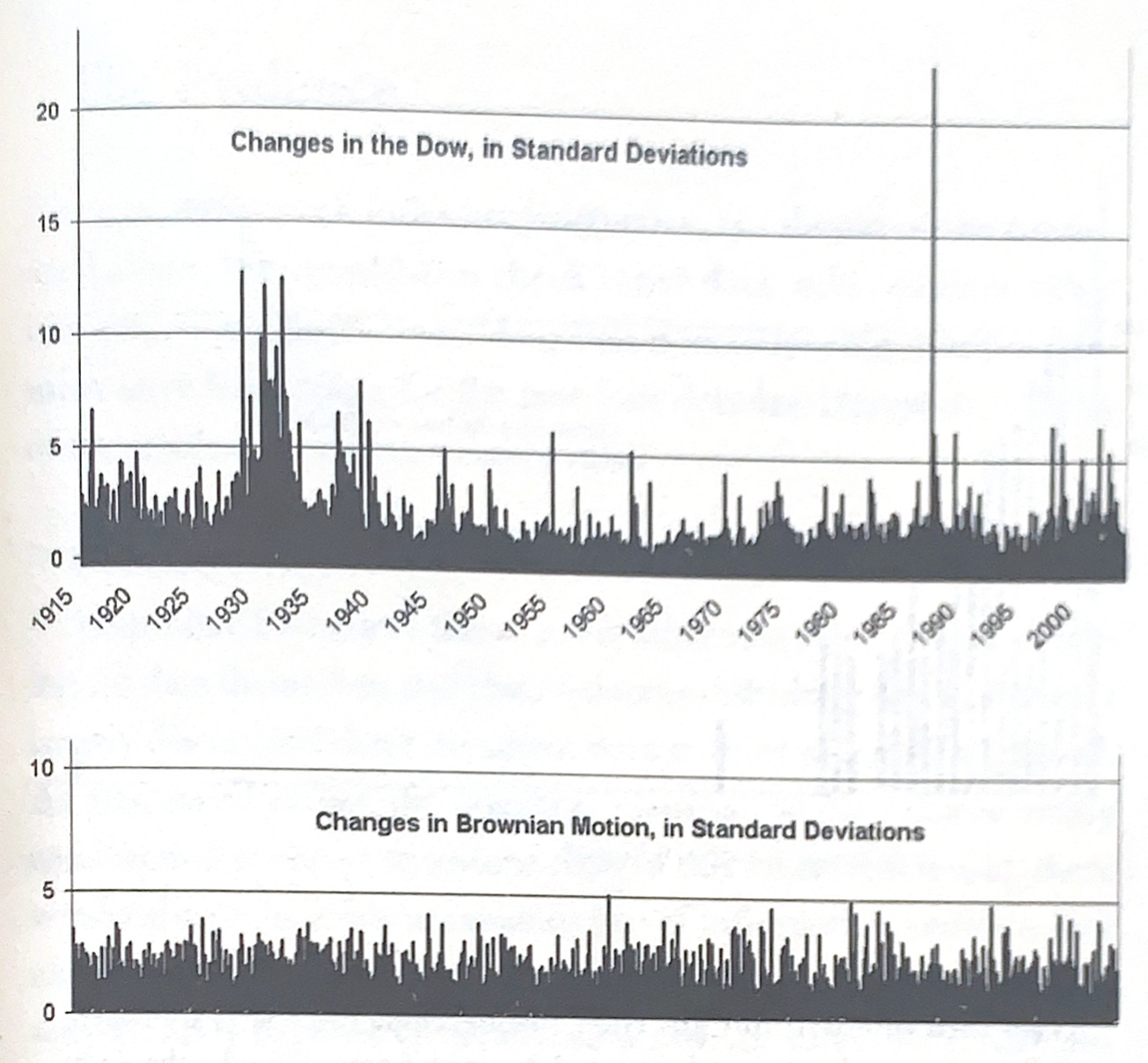

The bedrock of investment management, Modern Portfolio Theory (MPT), assumes that stock market returns follow a bell-curve. This unfortunately is not represented by reality, and markets can explode and implode every decade with probabilities measured to happen only a couple thousand years or worse.

“In the last fifty years, the ten most extreme days in the financial markets represent half the returns.” - Nassim Taleb in The Black Swan,

This theme of risk and return not following a bell curve is also referenced multiple times in Benoit Mandelbrot’s The Misbehavior of Financial Markets

1987: stock market crash and 1992 European interest rate moves were 22 sigma events, with odds of 1 in 10^100 (a googol, or 1 with a 100 zeros behind it)

2008: crash had odds of 1 in a billion

“Theory predicts six days of index swings [in the Dow Jones] beyond 4.5%; in fact there were 366. And index swings of more than 7% should come over every 300,000 years; in fact, the twentieth century saw 48 such days… perhaps, our assumptions are wrong” - Mandelbrot in The Misbehavior of Financial Markets

Bell curves can be useful for rough approximations, but I wouldn’t take a 25 year bet on it with literally ALL of my savings. Yet this is exactly what so many financial advisors encourage their clients to do.

The argument against maximizing savings

My whole point is that maybe this 25-29 year gamble is not worth it. Do you really want to work jobs that you hate or only kind-of like for 25 years, only to find out some economist’s models were wrong and you can’t retire yet? Would you want to be frugal that entire time, slaving away and living incredibly below your means? Even in our example, if you increased your contributions from $1,667 to $5,000 a month with 6% returns, it would still take you over 15 years to get to $1.5M [calculator]. Would you trade a quarter of your adult life for that?

If you poured your heart and soul into analyzing the markets, and contributed $5,000 a month and got an amazing 12% inflation-adjusted return, you’d still need 12 years. What about $10,000 a month with 12% returns? 8 years.

Compound interest takes time, and over a longer period of time you’re going to run into “black swan” events that happen every decade or so, yet go completely undetected by the standard model.

Some Afterthoughts On the Idea of Retirement

How would you find meaning in life if you didn’t need to work for an income?

A lot of people don’t stop to pause and think about what their retirement will actually look like. You might realize that your fantasy is just exactly that, a fantasy and not a real plan. Drinking margaritas on the beach every day might sound nice if you can never seem to catch a break, but it isn’t a sustainable thing to do for more than a couple weeks. Having a mega-yacht and helicopters is probably not in the cards for you - but if you manage to prove me wrong, congratulations. However, nearly all of the mega-rich will tell you that they got it through a combination of hard work AND luck (unless they are trying to sell you a book on how to get rich).

Another common retirement fantasy is travel. You many only be able to travel so much per year before it gets exhausting. I personally traveled for 50% of the time for a period of one year (half work, half pleasure) and it was incredibly fun but also incredibly draining. Further, authoritarian mandates and all out war are now commonplace. Good luck getting in or out of all the countries you want to see. Travel is fun, but it’s not a full time gig.

Summary

Getting an investment portfolio big enough to offset your monthly expense can take a very LONG time and the end date is NOT guaranteed.

Investment returns DO NOT follow a standard bell curve, yet every financial planner will try to trick you into thinking this way. You are exposed to far more risk than you think.

What would your retired life actually look like? Would you be content with it, or is it fantasy?

Disclaimer:

I’m some guy on the internet, and this is not financial advice. While substantial effort is made to be correct, some of the information presented may be wrong, estimates are not always accurate, and models can be wrong. Heck, my whole argument is that experts are capable of being wrong. The Author assumes no responsibility and will not be held liable for any damages that result from what you do with this information. You, the reader, are responsible for your own decisions and must do your own due diligence.

Appendix:

What Are Average Household Monthly Expenses in the US? Bank of America

U.S. Net Worth Statistics: The State of Wealth in 2023 | FinanceBuzzMedian Household

Mild vs. Wild Randomness: Focusing on those Risks that Matter Mandelbrot

About the Author

Nick Catranis is a modern portfolio theory apostate. He believes in personal freedom and prosperity.

Support

Send me an email! This is a new blog and all suggestions are welcome: subversivefinance@gmail.com

If you really liked my work, the biggest gift you could give me is spreading the gospel. Share it in r/personalfinance, twitter, linkedin, text it to your friends, whatever channels of communication you use.

I’m currently only on substack. Where else should I have a presence?